But the facts about MCOX do not support a case for fraud. A recent joint venture with Giosis, which is 49% owned by eBay (EBAY) and run by Gmarket's founder, Young Bae Ku, offers a turnaround opportunity. And at its current price, MCOX is trading below the cash value on its balance sheet.

This opportunity has arisen because most institutional investors have liquidated their positions in MCOX. This selling pressure keeps the share price low. However, I think the bearers have been overreacting on Mecox Lane's case.

Company Background

Mecox Lane Ltd. was founded in 1996. It was backed by venture capital firm Warburg Pincus since its inception. Warburg Pincus sold its entire stake to Sequoia Capital in 2008 for $80 million. Mecox Lane went IPO on the NASDAQ on October 2010. The IPO price was $55 per American Depositary Share. (It was actually $11, but the ADR ratio has changed from 1:7 to 1:35 share ratio).

Mecox Lane operates M18.com which sold apparel and accessories. Its target internet audience is women. But MCOX also has other sales channels, including a call center and physical stores (both franchised stores and direct-operated stores). Gross profit margin from Internet sales is just 20%, which is the lowest of the three sales channels. The internet channel faces fierce competition in China. So the company decided to scale down its advertising expense which resulted to revenue decline in 2011 and 2012. This is the reason the company decided to pivot its platform and turn M18.com over to the good hands of Giosis.

In comparison, Mecox Lane has 2 proprietary brands, Euromoda and Rampage - licensed from ICONIX (ICON) which its physical stores focus on selling. Mecox Lane also has proprietary brands for healthcare (MaxiCare) and cosmetics products (La Celler) that are sold through the call center. These sales resulted in a higher gross margin for the store and call center channels than for the internet platform channel.

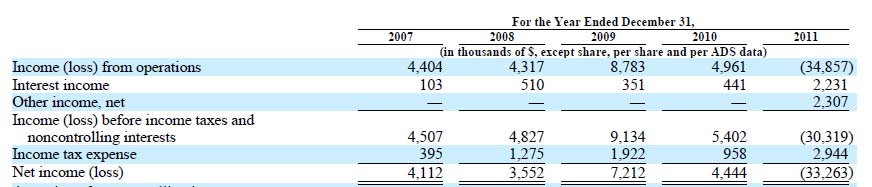

Since its IPO in December 2010, MCOX has suffered annual losses of over $55 million ($33 million 2011 and $22.4 million in 2012). The cause was the excessive competition in Chinese ecommerce space. The CEO of Mecox indicated in several conference calls that he was scaling down what he thought were absurdly high advertising fees. The reduced ad spending saved money, but resulted in a decline in revenue. The company also reduced spending by reduced the headcount. But the expenses still did not go down quickly enough. This resulted in operating losses despite declining operating costs. But prior to 2011, the company had been profitable. (See figure below which traced income back to 2007 from 20-F)

(click to enlarge)

Major Shareholders

Mecox Lane has very reputable majority shareholders, including SINA.com and Sequoia Fund. Most of the major shareholders hold shares at higher cost-basis than today's price. For example, SINA bought 18% of MCOX from Sequoia at $30 per ADS (ADR-ratio adjusted) in 2011. SINA puts $66 million in this investment which represents about 90% loss by current share price.

Most of Sequoia-backed Chinese IPOs (GAGA, CCSC and more) have suffered from low-valuation level since the IPO. But none of them have been a target of the short-seller. Sequoia is one of the biggest venture capital firms in the USA. Consequently, they might rush their portfolio companies to go IPO which force these companies to build business in unsustainable ways, such as excessive marketing expenses. But this aggressive stance does not make them frauds. Vipshop.com (VIPS) is a flash-sale website in China which made a debut last year in NASDAQ, and has made almost 300% gain from its IPO price at $6.5. Revenue of VIPS is growing rapidly but it is still operating at a loss. But it is still an impressive return in the stagnant market of Chinese companies on the US stock market.

My point is that internet business is one of easiest models to spot a fraud in. No one accuses VIPS or BIDU of fraud. So investors value these companies at fair price without a fraud's discount. MCOX, as the operator of M18.com, which is one of the leading ecommerce contender in China, deserves a better valuation from public market. But right now it is trading below cash per share, implying that investors are evaluating MCOX as if it were a fraudulent Chinese company.

Re-launching M18.com with partnership of Gmarket's founder and eBay

The recent JV announcement with Giosis to turn M18.com from an ecommerce website into an online market place platform also provided a vote-of-confidence and opportunity to turnaround this business. For this to happen, investors need to take some time and look at who Giosis is.

Giosis is the owner of Qoo10.com which is an online marketplace website serving major Asian countries. It is run by Mr.Young Bae Ku who is the founder of Gmarket.com, a South Korea internet company which was a Nasdaq-listed company that was sold to eBay for $1.2 billion in 2009. He later went to found Giosis to chase his ambition to make it big in Asia not just in South Korea. He moved his entire family to Shanghai to pursue an opportunity in China. That also showed the deep commitment he had in doing business in China. And 49% of Giosis also belongs to eBay. He then re-launched the new M18.com the 1st of January 2013. (Take a look at M18.com website now. It even has an eBay logo in the footer.)

(click to enlarge)

Giosis Mecoxlane is progressing rapidly. They have already launched a new M18.com app in both iOS and Android. I tried the iPhone version for about a week. They have new features within a couple of days. And last time I checked, they also had a lucky draw coupon which cost 1 RMB for each ticket to win an iPad Mini. The app is well-designed and easy to use and navigate.

The reason behind this JV is MCOX wants to exit the internet platform war and focus on making its own product lines. Also Giosis wants a strong brand, such as M18.com, to target female shoppers. M18.com will be the online marketplace for Women, not a general marketplace like Taobao or Qoo10.cn itself.

New Direction of Mecox Lane

The company has invested around $40 million in a new distribution center in Wujiang, which can handle 100,000 parcels a day. The CEO admits that the capacity is in excess of the company's current demand. However, the management is also planning to utilize the capacity as a 3rd party fulfillment service. The new M18.com as an online marketplace can act as a driver for this initiative.

Mecox Lane will be selling its own product line through a variety of internet channel, such as Tmall (Taobao) and Vipshop.com & Qoo10.cn (Giosis), as well as its new M18.com. Management expects this to save them on advertising expenses. The revenue from the internet platform is expected to decline in Q1 because the old M18.com also sells 3rd party products as 20% of total sale of their internet channel. But stopping 3rd party sales will improve the gross margin from internet sales. And free up some working capital.

The new JV (Giosis-Mecox lane) will be accounted for in equity method (MCOX invested $5 million and own 40% of the new JV). I expect the SG&A to decrease significantly because Mecox Lane can save by cuts to its huge online advertising cost. And the commission fee for using Tmall and the new M18.com will go to the selling expenses line. This is a much better business model, because commission fees for using other platforms is variable to sale volume.

Strong Balance Sheet and $10 million share buyback plan

The company announced $10 million share buyback plan on May 2012. Three quarters have passed since then, but it's only spent $572,000 in the buyback process. This is due to limitation on the buyback set by the US Securities and Exchange Commission. The company cannot buyback more than 25% of the 30-day average daily volume. Given that MCOX has sparsely traded, the company cannot buyback many of the shares. But the total outstanding number of ADS of MCOX is around 4 million (1:35 ADR share ratio) as of April 2012 (page 84, 2011 Form 20-F). So given the current price ($1.81) the buyback can still buyout all 4 million ADS outstanding.

At the end of December 2012, the company had $13 million in cash and $20.6 million in short-term investment which is in structured bank deposits equivalent to cash anyway. And $5 million to invest in the new JV is already booked as a prepaid expenses line. And there is no bank debt in both short-term and long-term. So, total equity is $89.9 million, while the current market capitalization is $21 million. It's trading at just 0.23x PB; and $21 million is even cheaper than total cash in hand.

CEO also owns a significant stake

Mr.Alfred Gu, the CEO, also own 18,364,525 ordinary shares which is about 5% of company. Additionally, he own 39 million options hence owning approximately 12.9 % of the company. An option has exercise price of $0.16/share which is equal to $5.6 per ADS. Major shareholders, such as SINA and China DongXiang (3818.hk), have a cost basis of $30 per ADS. Sequoia was able to cash out some share to SINA and DongXiang but still hold around 30% stake in MCOX. Another management staff has the option to purchase MCOX's ADS at $5.6. It's fortunate that public investors can gain entry at such significant discounts compared to major firms and insiders. Private investors should see from these actions, and the existing balance sheet, that MCOX is not the fraud they feared it was.

Going Forward

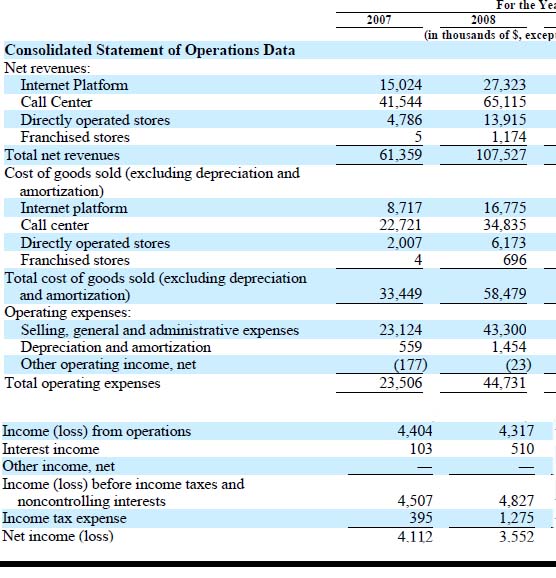

If the company succeeds in reducing expenses, and scales down the low-margin business segment, and scales up the higher margin business segment (the call center segment, which does most of its sales from Health Care and Beauty products, and currently attains close to 60% gross margin), I believe Mecox Lane can become profitable again. Look at the income statement for the year ended 2007-2008 which were the pre-Sequoia days. (See figure below) The revenue came mostly from call center. And the company had a net income around $3.5 million.

(click to enlarge)

Many investors have been abandoning ship lately, especially Chinese ships. However, at the current price, which is less than the total cash value per share, MCOX is not only a safe buy, but also a safe way to go to earn investors a nice return within just a few years. Just like Monnish Pabrai said, "Heads, I Win; Tails, I Don't Lose Much" But in this case, I might say "Heads, I Win Big; Tails, I Don't Lose At All."

No comments:

Post a Comment